deferred tax asset and liability

cfa | tax income

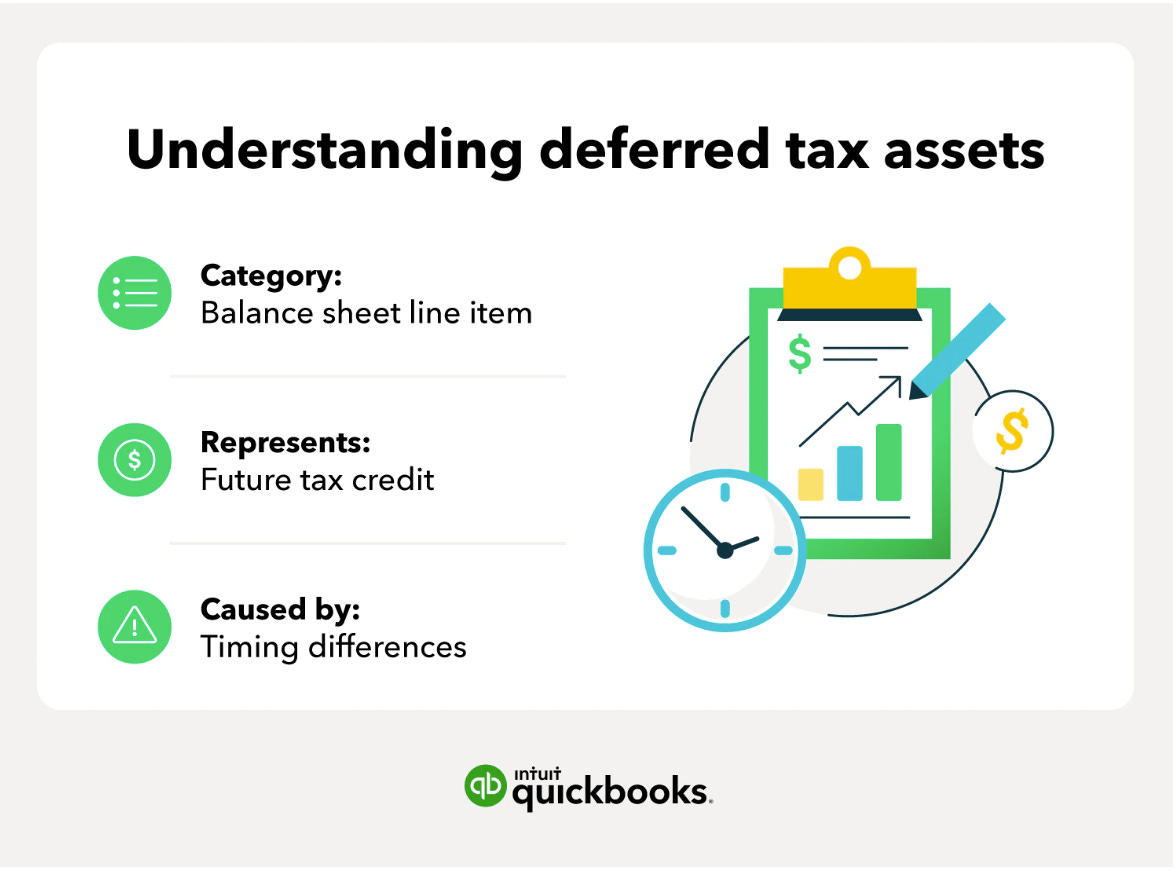

A deferred tax asset is a business tax credit for future taxes,

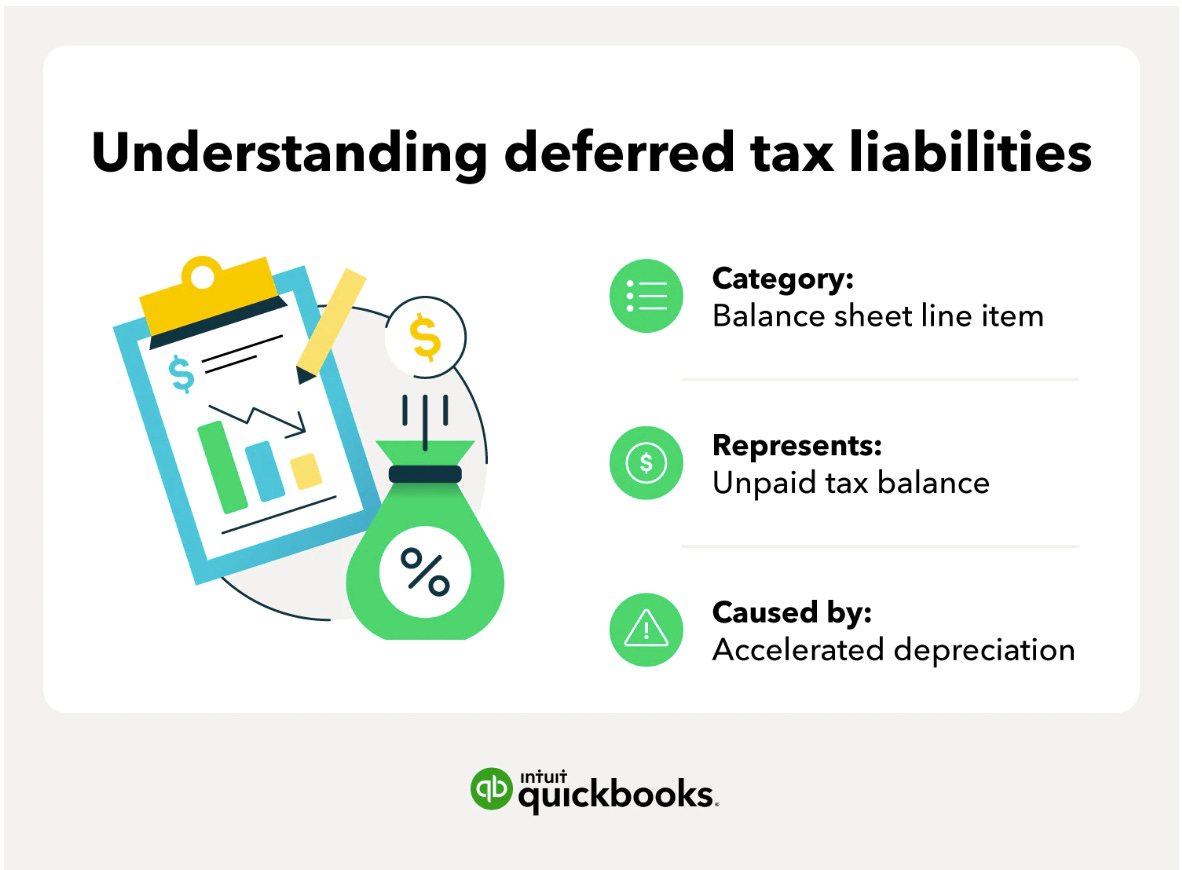

and a deferred tax liability means the business has a tax debt that will need to be paid in the future.

You can think of it as paying part of your taxes in advance (deferred tax asset) or paying additional taxes at a future date (deferred tax liability).

Khi mình đã trả thuế sẵn trước cho tương lai thì tương lai sẽ không phải trả phần này nữa. Phần trả trước này được coi là tài sản (asset), hoãn lại cho tương lai (deferred)

Khi mình hoãn việc nộp thuế lại, bây giờ trả một phần sau này trả phần còn lại thay vì trả hết theo lý thuyết (tax expense - financial accounting); thì phần hoãn lại cho tương lai này gọi là deferred tax liability.

A deferred tax asset (DTA) is an entry on the balance sheet that represents a difference between the company’s internal accounting and taxes owed. For example, if your company paid its taxes in full and then received a tax deduction for that period, that unused deduction can be used in future tax filings as a deferred tax asset.

Ví dụ năm đó bạn đã trả thuế đủ nhưng đột ngột có chính sách giảm thuế; thì phần bạn đã trả dư sẽ được coi là Deferred tax asset. Được bảo lưu cho tương lai.

DTA: financial asset; non-current/intangible on balance sheet

What type of asset is a deferred tax asset? A deferred tax asset is considered an intangible asset because it’s not a physical object like equipment or buildings. It only exists on the balance sheet.

Is a deferred tax asset a financial asset? Yes, a DTA is a financial asset because it represents a tax overpayment that can be redeemed in the future.

Where are deferred tax assets listed on the balance sheet? They are listed on the balance sheet as “non-current assets.”

When does a deferred tax asset have to be used? Deferred tax assets never expire, and can be used whenever it’s most convenient to the business.

Deferred tax liability

A deferred tax liability (DTL) is a tax payment that a company has listed on its balance sheet, but does not have to be paid until a future tax filing.

DTL là 1 dạng thuế được hoãn lại. non-current liability.

Hơi giống việc mình đi mua mít, đã đồng ý trả 10k nhưng đang tạm hoãn lại chưa trả.

DTA: tax overpayment

DTL: tax underpayment

Formula:

Income tax expense = taxes payable + deferred tax liability – deferred tax asset

deferred tax asset » positive cashflow

Differences in depreciation methods for book income and taxable income generate temporary differences.

Tổng số tiền thuế phải trả sẽ bằng nhau; chỉ có thời điểm trả tạo ra sự khác biệt tạm thời thôi.

DTA is presented under non-current assets and DTL under the head non-current liability.